JustEat Takeaway Merger Prospectus (TKWY + GRUB)

JustEat Takeaway Merger Prospectus (TKWY + GRUB)

The original restaurant marketplaces are merging to take on new competitors.

DISCLAIMER: This newsletter reflects my opinions and should NOT be considered investment advice. I do my best to ensure the accuracy of information included in the newsletter at the time of writing, but these companies and markets change rapidly and I make no promise to the timeliness, or accuracy, of the information presented. Investing in equities mentioned in this article carries risk, including the loss of principal. Please do your own research.

Summary

Just Eat Takeaway (JET) & Grubhub, founded in 2000 and 2004 respectively, are merging to form a global food delivery company with a market-leading position across Europe and a presence in the US, Canada, Brazil, Colombia and Australia

The combined business is valued at a little over €15B, and generated about €4B in revenue (of which €1.5B was paid out to drivers) and also includes a 33% stake in Brazilian food deliver company iFood valued at over €2.3B

Grubhub has lost market share over the last several years, as delivery logistics firms DoorDash and Uber Eats became the dominant players in the US market. This loss of market share in the US accelerated in 2020.

JET has successfully fought back in Europe due by subsidizing the delivery operation with the favorable unit economics of its marketplace business. It is possible that increasing regulations on gig-economy workers position JET to maintain market leadership in Europe, and recapture share in the US.

Background

In June 2020, JustEat Takeaway acquired Grubhub in an all stock transaction that valued the company at $7.3B USD. This came on the heels of a £6.2B acquisition of JustEat, another market-leading European delivery company, by Takeaway.com. Together, these companies make up the old guard in the food delivery space, and their rapid consolidation in 2020 comes in response to the growing threat of delivery logistics companies such as DoorDash, Uber Eats, Deliveroo and Delivery Hero.

Jitse Groen, the current global CEO of JET, founded the company in the Netherlands in 2000, and began international expansion within Europe in 2007. However, Takeaway.com didn’t start building its delivery business until 2016, the same year it held its initial public offering. In recent years, the company has expanded aggressively through acquisitions acquiring Just Eat (UK) and now Grubhub (US) among others. After the acquisition Grubhub CEO Matt Maloney will stay on at JET’s North American CEO overseeing Grubhub and Canada’s SkipTheDishes.

As the delivery-first entrants came to market they were able to offer a wider variety of foods (especially from QSR restaurants like McDonalds or Wingstop). This accelerated churn for the incumbents who retaliated with their own delivery networks, though Jitse insists that the JET delivery business is “gross-profit neutral” and the company extracts its earnings power from its pure-play online marketplace customers.

Market

Much of the market summary for Just Eat Takeaway (JET) is duplicative of what’s already been covered in the Doordash S1 Teardown (so check that out if you haven’t yet). The major difference, however, is the truly international footprint of JET. The company currently operates in 23 markets: the United Kingdom, Germany, Canada, the Netherlands, Australia, Austria, Belgium, Bulgaria, Denmark, France, Ireland, Israel, Italy, Luxembourg, New Zealand, Norway, Poland, Portugal, Romania, Spain, and Switzerland, as well as through partnerships in Colombia and Brazil. With the addition of Grubhub, they’ll add the US market to their list.

DoorDash, on the other hand, only competes in the US, Canada, and Australia for the moment. Though job postings for DoorDash reveal that the company is planning to establish a base of operations in Berlin, signaling that European expansion is just around the corner.

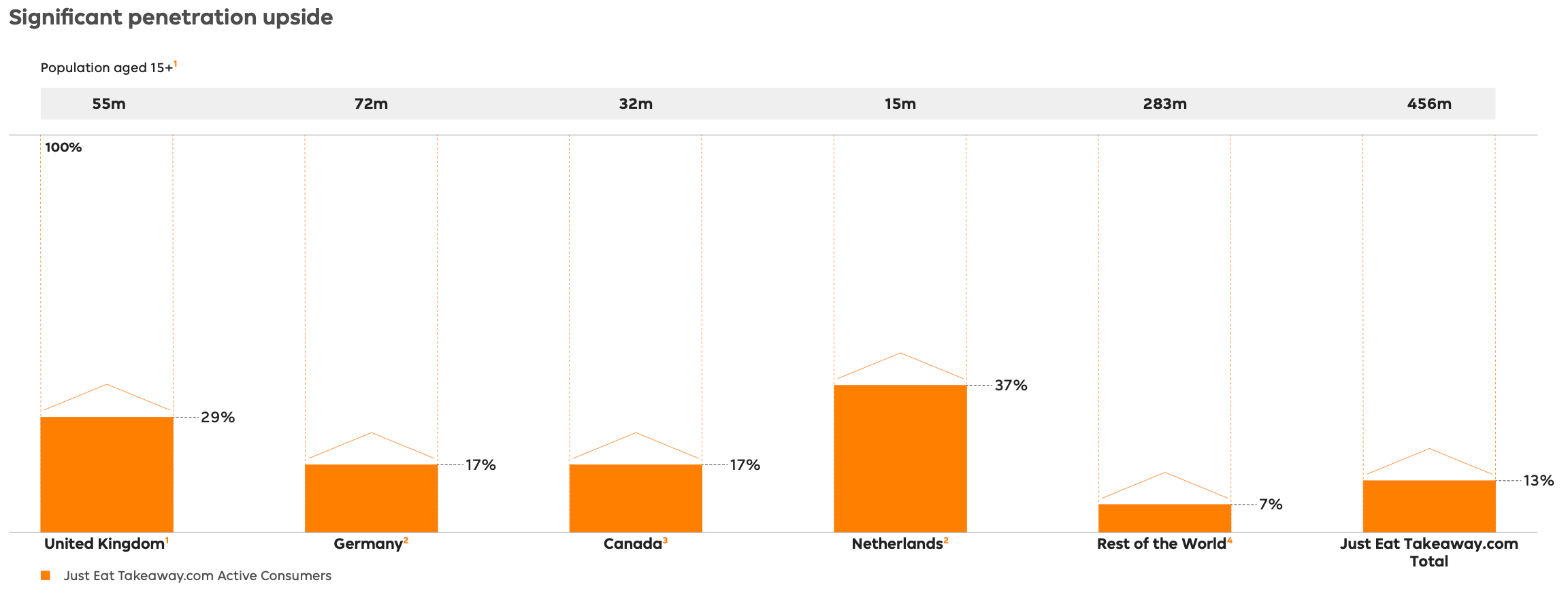

Just Eat Takeaway has a leading market position in several large European markets, but believes that there is still significant room for expansion. The company estimates it has only penetrated about 40% of the addressable market in its most mature market (Netherlands) where it began operations way back in 2000.

Unit Economics

Business Model

As mentioned earlier JET represents the old-guard of the food delivery business which means its core (and profitable) business is online ordering, not delivery logistics. JET refers to this online ordering business as marketplace and uses the metric delivery share to outline the proportion of its orders derived from delivery.

Total Orders = Marketplace Orders + Delivery Orders

Delivery Share = Delivery Orders / Total OrdersIn 2020 26% of JET’s business is based on the delivery model, which increased from 18% in the year prior. Here’s the country-by-country breakdown of JET delivery share:

In both business models (delivery/marketplace) JET earns revenue as a percentage of GMV. However, Grubhub/JET include delivery costs in Revenue, which makes them slightly difficult to compare with DoorDash. To make this comparison simpler, I’ve decided to focus on Revenue excluding courier costs here.

Excluding courier costs, JET earned €1.3 in Revenue during 2020 which is roughly 10% of GMV for the same period (€12.9B). In the pro-forma statement of operations, we also learn that Grubhub delivery expense (previously bundled together with operations/support costs in SEC filings) were $727M (€638M * 1.14 exchange rate). Excluding delivery costs, Grubhub revenue would be $1.1B implying a roughly 12.5% take rate on $8.66B in Gross Food Sales.

Demand

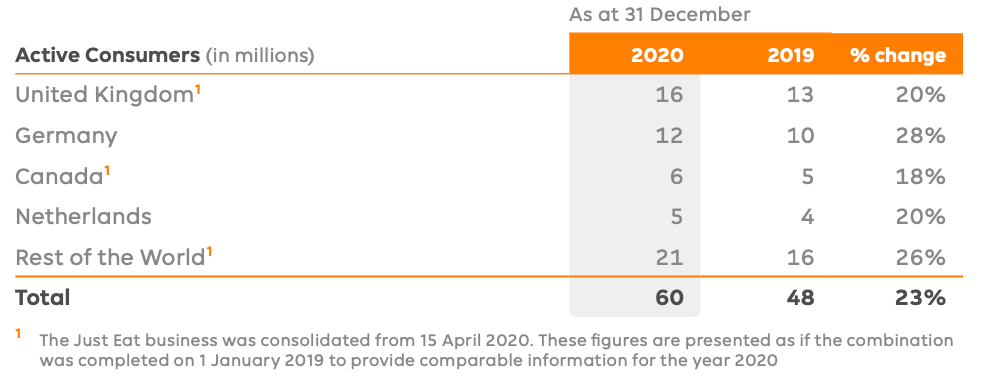

JET and Grubhub consider an Active Consumer as anyone who has ordered in the past 12 months1. In 2020, these businesses connected over 90M consumers with restaurants nearby (60M JET; 31M GH). Here’s the country-by-country breakdown of Active consumers for JET:

In total, JET users placed 588 million orders at an average order value of 22 during 2020, but new users of the service are much more likely to churn, resulting in lower order frequency. JET highlights an average order frequency for returning customers of 15.2 implies an average revenue per returning user of €42 (€22 AOV * 15.2 order frequency * 12.5% take rate). JustEat spent €369M in marketing implying a CAC of ~$30 per incremental active user, or ~$40 per incremental active returning user, for a payback period of about 12 months.

In 2020 Grubhub spent $400M on marketing to acquire an incremental 8.8M active diners implying a roughly $45 CAC. All-in-all order frequency and the unit economics of Grubhub seem extremely similar to JET, which (while profitable) seem inferior to DoorDash. Higher order frequency, and higher LTV as a result, give DoorDash a greater willingness to pay for a new customer, a likely reason that DoorDash was able to take market share so rapidly.

Supply

JET already connects its users to 244k restaurants and with the addition of Grubhub will expand that number to roughly 500k. More importantly to point out, is the way that JET manages its delivery operations. JET also supports two employment models for its couriers:

Scoober - a delivery model in which JET employs its couriers and provides them with benefits; currently live in 12 markets and employing 20k couriers

Delco - a delivery model pioneered by acquired Canadian firm SkipTheDishes, in which couriers are employed as independent contractors (similar to Uber/DoorDash); currently live in 5 markets employing 157k couriers

While I can imagine it’s a pain to support the two models simultaneously, because they operate in many different legal jurisdictions JET has been forced to ramp on the systems/processes that are becoming requirements in more and more countries and is quickly making the transition to Scoober in jurisdictions like Spain and Italy. This gives JET a significant operational head start on their competition, but it also gives investors some visibility into long-term margins at JET.

Valuation

Price

At the completion of the acquisition, Grubhub shareholders will own roughly 1/3 of the combined JustEat Takeaway + Grubhub entity and there will be just under 214M shares outstanding. The combined entity will be in a roughly cash-neutral position (debt = cash), so the current share price of €72.40 implies an enterprise value of €15.5B.

To put the valuation in context, I decided to look at revenue exclusive of courier costs, to make this a fairer comparison with Doordash:

1x EV / GMV (€15.1B = €12.9B JET + $8.6B GH * 1.22 exchange rate)

6.2x EV / Revenue excl. Courier Costs ($2.5M = €4B Rev - €1.5B Courier Costs)

€31x EV / Restaurants (500k = 245k JET + 265k GH)

€170 EV / 2020 Active Consumers (91.5M = 60M JET + 31.4M GH)

Finally, JET holds a 33% stake in Brazilian food delivery giant iFood. In the most recent annual report, management discussed that they’ve received inbound interest for their stake in the company with a highest bid of €2.3B, though the company believes the stake is worth more. This means that JET values its stake in iFood at 20% or more of their current enterprise value.

Growth

We’ll look at GMV growth rates to focus on the rate at which the business is growing share in the takeaway industry. Focussing on Revenue can be inconsistent as it’s skewed by changes in delivery share. In 2020, JET did just a €12.9B in GMV, an increase of 51% from the year prior. Grubhub did of $8.6B in GMV, up 47% Y/Y.

It is likely that this growth rate rate will slow considerably over the next year. GMV at Grubhub increased just 17% from 2018 to 2019 under pre-pandemic circumstances. The merger prospectus does include a forward revenue projection for the JustEat Takeaway business, which was used during diligence. This projection showed a steady 20% CAGR from FY2020 to FY2024 leading to a doubling of revenue over 4 years.

Both businesses saw an acceleration of GMV growth in Q1 ‘21 vs Q1 ‘20 (JET 88%; GH 53%), but this is unlikely to persist at current levels. Given this, I think we should expect a post-pandemic GMV growth rate of roughly 30%.

Profitability

JustEat and Grubhub have been operating at breakeven cash flow and reinvesting cash into expansion for the past several years. In fact, JET never took on outside funding until 2012, over a decade since the company was founded. This is a significantly different approach compared to competitors DoorDash and Uber who have burned huge amounts of investor capital to rapidly achieve scale.

The combined entity will have €822M in cash and equivalents offset by €872M in borrowings. Gross margins are materially better than DoorDash at nearly 80% (€2.5M Rev excl. Courier Costs - €500M order processing costs / €2.5M).

The company breaks out Adjusted EBITDA across its key geographies, which gives us some visibility into profitability in core markets. Notice that Canada has just 10% EBITDA margins, as it is a 100% delivery Market, while The Netherlands boasts a 44% EBITDA margin by sourcing 93% of its orders from marketplace.

Color Commentary

The Grubhub merger gives JET access to the world’s largest food delivery market, but hasn’t gone according to plan. To understand the current prospects of JET, you must first understand the intention of the merger. Here’s a video of Grubhub CEO Matt Maloney explaining the decision:

Specifically, I’d like to call out two quotes, which comes at the 3:30 and 5:00 marks.

1) We are winning back share…

Grubhub did not “win back share” in 2020 as he asserted, but continued to fall further behind. Grubhub grew just 50% Y/Y while DoorDash grew 200% and Grubhub ended the year at just 1/3x the GMV runrate of their competitor.

2) We are the most valuable asset in the world, because we are the only profitable player in the world’s largest food delivery and takeout market.

Thanks to world-class execution over the past 12 months, DoorDash finished Q1 ‘21 with positive operating cash flow, and guided for 0-300M in Adjusted EBITDA for FY ‘21, as it grows about 40% Y/Y. So, it appears that DoorDash has crushed Grubhub, and has the cash to continue to pull it off.

This doesn’t mean that Grubhub can’t fight back, nor that DoorDash can translate its success to JET’s profitable European markets, but for now at least it seems like the delivery-first model has eaten Grubhub’s lunch in the US.

Despite Grubhub’s US struggles, JET may have a structural advantage in Europe. JET has gone head-to-head with delivery-first businesses like Delivery Hero (Germany) and Deliveroo (UK) and come out on top in key European markets. Last week, Delivery Hero announced their intention to re-enter the German market after selling its operations to JET in April 2019. Jitse didn’t mince words in his response:

It is possible, especially in countries with more regulation on gig-economy workers, that JET still has a superior business model. The risk for Uber/DoorDash is that these regulations will eat away at their delivery margins, leaving JET and Grubhub in a superior competitive position. If so, DoorDash will face an uphill battle against JET in Europe and Grubhub could re-emerge as a competitor as gig economy legislation makes it way through the US.

Germany may decide the future of food delivery. With Delivery Hero’s reentry into the German market, and DoorDash setting up an office in Berlin, it appears that Germany will be the next front of the food delivery war. JET is the market leader, and employs German couriers as a part of its Scoober delivery model. Furthermore, JET is planning to roll out grocery delivery in the country as a test to bolster its position. This comes as an abrupt change of heart as Jitse said the company had no intentions to get into grocery delivery as recently as their most recent earnings call on March 10.

In the coming quarters, I’ll be looking for a couple things in Germany:

Will JET delivery share accelerate in Germany to defend against competition?

Will delivery (and grocery) in Germany lead to higher order frequency for JET?

Will DoorDash adopt employment models in any European countries, or stay firmly rooted in places where they can keep dashers as independent contractors?

The valuation for JET is attractive compared to other marketplaces. Unlike the other 3 businesses I’ve analyzed (Rover, Airbnb, DoorDash), if you can get comfortable that JET is a long-term winner in the space; you don’t need to pull forward years of growth to validate the current valuation. Adjusted EBITDA is temporarily suppressed as the company invests in international expansion, but if you believe in the long-term 25%+ Adjusted EBITDA margins in mature countries, the earnings power of €4B in GMV is already above €1B2. If you exclude the €3B stake in iFood from the Enterprise value of €15.5B you are left paying 10-12x earnings power, far cheaper than any of the other businesses I’ve analyzed thus far.

The big question that remains is whether that earnings power is real, or will be perpetually competed away by competition.

Thanks for reading! If you enjoyed this please consider sharing this article, and don’t forget to subscribe to receive analysis on other marketplace businesses. Let me know in the comments what you think about JET, or or hit up @marketmkrs on twitter!

Note this is a different definition compared to DoorDash which reports consumer numbers as active in the past month (most recently 20M in December ‘20)

This is obviously a crude method of valuation, but I assume that the current base of revenue €4B can generate at least €1B (€4B * 25% Adj. EBITDA MARGIN) in Adjusted EBITDA if the team were to stop prioritizing market share growth, and focused on profitability.